yahoo Press

What is a dependent care FSA?

Images

1 / 12

2 / 12

3 / 12

4 / 12

5 / 12

6 / 12

7 / 12

8 / 12

9 / 12

10 / 12

11 / 12

12 / 12

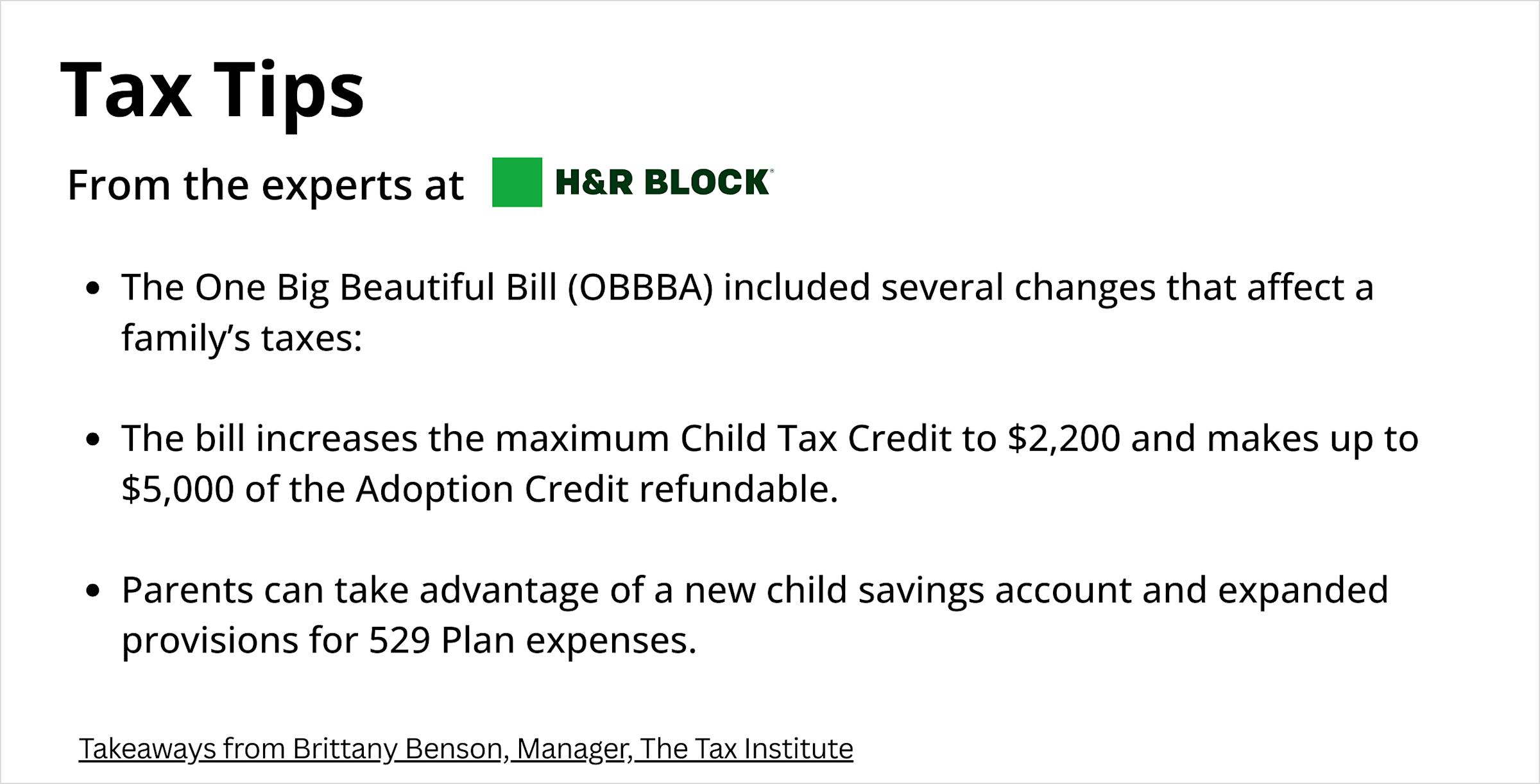

A dependent care flexible spending account (DCFSA) is a tax-advantaged account that lets you build tax-free savings for adult and childcare expenses. It’s a nice perk, but it requires some planning and follows certain rules. DCFSAs are part of many employer benefits packages or cafeteria plans. You can sign up for an account during open enrollment or a qualifying life event and choose how much to contribute from each paycheck. Your employer may give you a debit card to pay for eligible expenses, or you can pay out of pocket and submit a claim for reimbursement. To be eligible for dependent care benefits, you have to work for an employer that offers a DCFSA and meet IRS requirements for claiming dependent care expenses, including the following: The expenses must cover caring for a child under 13 or a spouse or dependent who cannot care for themselves. You (and your spouse if filing jointly) have earned income during the year. You’re paying for care so you can work or look for work. Funding your DCFSA with pretax money lowers your taxable income and, ultimately, your tax bill. For a married couple in the 22% federal tax bracket, tax savings from a dependent care FSA could total more than $1,100 if they contribute the maximum of $5,000 (the 2025 limit). That amount goes up for tax year 2026. Depending on your employer, you may be able to save up to the annual contribution limit of $7,500 (or $3,750 if you’re married and filing separately) for 2026, up from $5,000 for 2025. However, these are federal limits, and employers are not required to match them. So make sure you understand the limits with your specific plan. Aim to use your DCFSA funds by the end of the plan year, or you’ll forfeit them to your employer. Employers can offer a 2 ½-month grace period during which you can continue to incur and claim approved expenses. Talk with your human resources group or check your employee benefits plan for specific details. The dependent care FSA contribution limit increased in 2026, but how much you can save depends on your tax filing status. Single or head of household: $7,500 Married, filing jointly: $7,500 Married, filing separately: $3,750 Since you have to set your contribution amount for the year ahead of time — usually during open enrollment — you’ll have to do some planning. Estimate your 2026 expenses by looking at what you spent in previous years or adding up monthly fees for your children’s preschool, for example, to determine how much you should save. Remember, you forfeit unused FSA funds at the end of the calendar year. Expenses are FSA-eligible if they are work-related, meaning they’re costs you pay for the care of a qualifying dependent so you can work or look for work. Examples of dependent care FSA-approved expenses could include: Day care, preschool, or similar programs. A babysitter, au pair, or nanny who watches your child while you work. Before- or after-school programs and summer day camps. Dependent care centers, like adult day care. Some expenses that are not FSA eligible include private school tuition, overnight camps, and music lessons or sports programs. You may be able to combine dependent care tax breaks with other tax benefits to maximize your tax savings. Consider these additional savings for households with children or dependents. Child tax credit: The child tax credit is a tax break for households with kids under 13. You can claim this credit, worth up to $2,200 per child for 2025, even with a DCFSA. Child and dependent care tax credit: The child and dependent care tax credit lowers your tax bill based on what you paid for dependent care. Because the DCFSA and childcare credit cover similar expenses, you can use both as long as you don’t claim the same expenses for both benefits. Households can claim up to $3,000 for one dependent or $6,000 for two or more dependents. A dependent care FSA is one of several savings accounts with tax benefits. Here are two others worth noting. Healthcare FSA: Use pretax money to save and pay for eligible health expenses through a healthcare savings account only available through your employer. Health savings account (HSA): Like an FSA, you can use an HSA to save for medical expenses with pretax dollars, but only if you’re enrolled in a high-deductible health plan. You don’t need an employer to open an HSA, and there is no annual deadline to use the funds. Learn more: FSA vs. HSA: Which account is better for you? Your dependent care FSA balance does not roll over. Unused funds usually expire at the end of the year unless your employer offers a grace period of up to 2 ½ months into the new year. FSA-eligible expenses are for qualifying adult or childcare that allows you to work or look for work. These programs could include elder care, babysitting, nursery school, and before- or after-school care. You can use a dependent care FSA with the child tax credit. The child tax credit gives up to $2,200 per qualifying child. You may also be able to combine your FSA with the child and dependent care credit, which is a tax break for dependent care expenses. The dependent care credit provides $3,000 for one dependent and $6,000 for two or more dependents. You can’t claim expenses already reimbursed through your FSA. Learn more about the child and dependent care tax credit, including how to qualify and what it’s worth. HSAs and FSAs let you save for eligible medical expenses with pre-tax dollars. Learn the details of each to decide which account is best for you. A health savings account is designed to help people on high-deductible healthcare plans pay for medical expenses. However, there are important health savings account rules to keep in mind, and not everyone qualifies to open an HSA. Learn more. Learn how the child tax credit changed for the 2025 tax year, who's eligible, how much it's worth, and how to claim it on your federal tax return. One often overlooked way to save money is taking advantage of employer benefits and perks. Find out if your job offers any of these programs to help save money. Both a health savings account (HSA) and a high-yield savings account (HYSA) can help with medical expenses. But they work very differently. Here’s how to choose.