yahoo Press

Middle East conflict: An initial impact assessment on Automotive

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

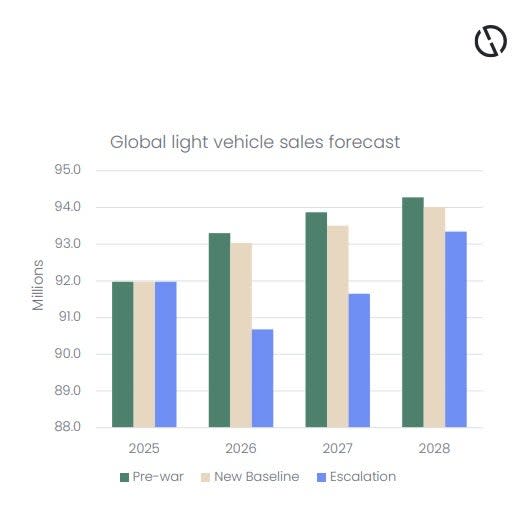

The escalating war between the US, Israel, and Iran is creating the most severe disruption to global energy markets since the 1970s. The effective closure of the Strait of Hormuz has pushed oil prices briefly above $110 per barrel within days, while the shock is spreading to shipping, aviation, and trade, raising global recession and inflation risks, according to GlobalData, a leading intelligence and productivity platform. The most immediate macroeconomic impact is being transmitted through energy supply and maritime shipping. The Strait of Hormuz is effectively closed to most traffic after Iranian threats and tanker attacks, leaving nearly 200 vessels stranded. Markets have repriced rapidly: oil has jumped from roughly $70 to above $110 per barrel in days, while Asian LNG spot prices have more than doubled. Higher fuel costs are feeding directly into transportation and distribution, with US diesel reaching a two-year high of $4.04 per gallon—raising the probability of renewed inflation pressure across multiple economies. The latest developments in the Middle East will add weight to demand downside risk as global economic growth is squeezed by higher than previously expected price inflation and interest rates. Consumer and business confidence will take a hit if the war persists. Stock markets have lost significant value already. Any hit to economic growth will negatively impact underlying demand in automotive markets, with associated implications for profitability all along supply chains. Squeezes to real incomes caused by higher-than-expected price inflation and interest rates will influence purchase decisions as will higher finance costs. There will also be higher costs in materials and manufacturing that will be difficult to pass on to the final consumer, adding to pressures on profitability. The Middle East region itself is directly and immediately impacted. For 2025, the Middle East Light Vehicle (LV) market is estimated to have sold 3m units, of which a third can be attributed to sales in Iran. Other major players include Saudi Arabia, the UAE, and Israel. This year, the Middle Eastern outlook was initially one of growth as sales have been following an upward trend across the region in recent times. However, as the situation regarding the Iran War is developing quickly, the analysts at GlobalData have taken a more cautious stance on the LV forecast for 2026. For 2026, GlobalData has lowered its Middle East LV forecast by 12.5%, from 3.1m units to 2.7m units. Roughly half of this revision is driven by a downward adjustment to our Iran LV forecast, which is down 20% from 950k units to 760k units. GlobalData analysts stress this is an initial first-pass, and the risk to the regional forecast is clearly greatest here. The situation remains fluid, and continued volatility is likely to strain consumer confidence, business sentiment, and cross-border trade activity in the near term. For the automotive sector, this typically translates into delayed purchases, tighter credit appetite and greater caution among fleet operators and distributors. OEMs and dealers may also face higher logistics and insurance costs, as well as greater difficulty forecasting demand and managing inventory. The baseline global LV forecast of growth in 2026 remains intact, at this stage. That is, GlobalData sees a market climbing from 92m vehicles in 2025, the best year this decade, to 93 m vehicles sold this year. While downward adjustments have been made since the conflict began, amounting to around half a million units for 2026, the focus has been on the Middle Eastern markets themselves, and the sizeable market of Iran, in particular. Elsewhere, the focus of any significant reductions in the LV markets in other regions will primarily come from the economic drag due to an energy-price shock. Disruption of the supply channels for oil and gas in the region is already impacting prices of those commodities. This will inevitably lead to some feed through into CPI elsewhere, including, but not limited to, Europe and North America. Added to this, higher inflation would apply pressure to interest rates, whether that be slowing the decline or reversing monetary easing. Meanwhile, the costs associated with vehicle production will also climb. All of this is an added headwind to vehicle sales. All of that said, at this stage, the baseline forecast assumes that such an energy price shock would be fairly limited in nature. However, an escalation in the energy crisis, through higher prices still and a longer timeline of reversion to lower levels, could have somewhat stronger implications for the LV market. GlobalData puts the risk in the order of 2-3m vehicles this year in such an event, with the drag carrying through for the next few years. The Middle East conflict comes at a time when the auto industry is already facing significant industrial and commercial pressures. These include the cost of technological transition, new protectionist tariff policies, DRAM chip supply challenges, lacklustre demand in core markets, and enduring vehicle manufacturing overcapacity. Aside from the direct impact on vehicle demand in the Gulf Cooperation Council (GCC) economies, the increase in global energy prices will add another layer of cost pressure to the auto industry’s highly energy-intensive supply chain. Steel and aluminium make up a significant proportion of vehicle and powertrain composition. Steel foundries and aluminium smelters are amongst the most energy-intensive processes. In addition, plastic and polymer components are also widely used in all vehicles, and this content is almost entirely petrochemical in origin. Military threats within the Strait of Hormuz and transit constraints elsewhere are already adding cost to logistics, with Drewy Maritime research highlighting a trebling of Very Large Crude Carriers (VLCC) rates in March since the start of 2026. Much depends on the timeline development of the conflict. While at this stage most are assuming a short duration of disruption, there is potential for wider escalation with significant and enduring ramifications for deeper pressure on an already challenged auto industry. "Middle East conflict: An initial impact assessment on Automotive" was originally created and published by Just Auto, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.