yahoo Press

Tyler Technologies’ Q1 2026 Earnings: What to Expect

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

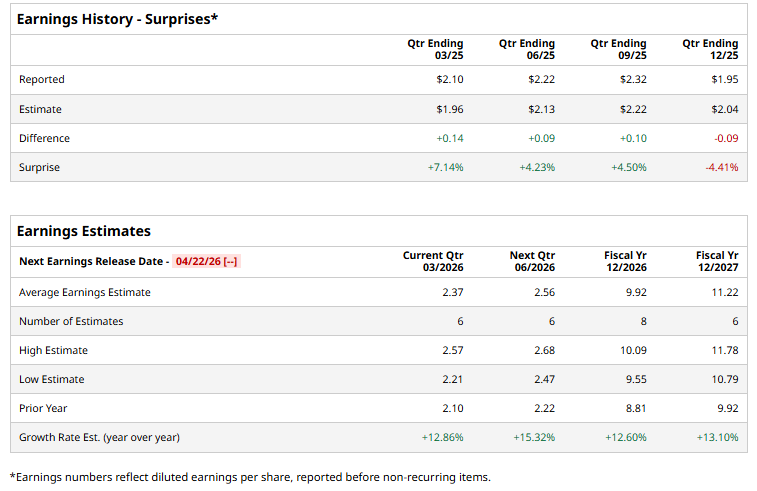

Texas-based Tyler Technologies, Inc. (TYL) is a leading provider of integrated software and technology services for the public sector. With a market cap of $14 billion, the company's client base includes local government offices throughout the U.S., Canada, Puerto Rico, and the United Kingdom. The software giant is expected to announce its fiscal first-quarter earnings for 2026 in the near term. Ahead of the event, analysts expect TYL to report a profit of $2.37 per share on a diluted basis, up 12.9% from $2.10 per share in the year-ago quarter. The company has surpassed Wall Street’s EPS estimates in three of its last four quarterly reports, while missing the mark in one. META Stock Just Had Its Worst Day in Nearly a Year. Here's What Happened. The Strait of Hormuz Crisis Provided a Temporary Distraction from a Collapse Brewing in AI Stocks. What Comes Next Could Get Ugly. Why Is SanDisk (SNDK) Stock Down Today and Should You Buy the Dip? Stop Missing Market Moves: Get the FREE Barchart Brief – your midday dose of stock movers, trending sectors, and actionable trade ideas, delivered right to your inbox. Sign Up Now! For the current year, analysts expect TYL to report EPS of $9.92, up 12.6% from $8.81 in fiscal 2025. Its EPS is expected to rise 13.1% year over year to $11.22 in fiscal 2027. TYL shares have dipped 40.9% over the past year, notably underperforming the S&P 500 Index’s ($SPX) 13.4% gains, and the State Street Technology Select Sector SPDR Fund’s (XLK) 24.1% gains over the same time frame. Tyler Technologies got a boost on Feb. 17, with shares climbing 2.8% after D.A. Davidson’s Peter Heckmann reaffirmed a “Buy” rating and set an ambitious $460 price target, reinforcing bullish sentiment around the stock’s growth trajectory. Analysts’ consensus opinion on TYL stock is very bullish, with a “Strong Buy” rating overall. Out of 22 analysts covering the stock, 16 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and five give a “Hold.” TYL’s average analyst price target is $452.90, indicating an ambitious potential upside of 32.8% from the current levels. On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com