yahoo Press

Willis Towers Watson's Q1 2026 Earnings: What to Expect

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

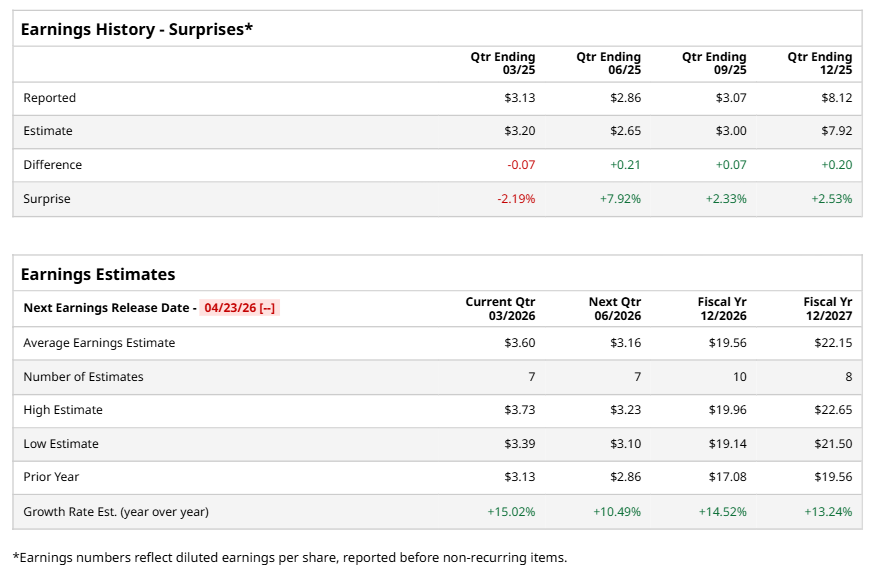

London, the United Kingdom-based Willis Towers Watson Public Limited Company (WTW) operates as an advisory, broking, and solutions company worldwide. Valued at $27.4 billion by market cap, the company provides a range of insurance brokerage, reinsurance, and risk management consulting services. The leading global advisory, broking, and solutions company is expected to announce its fiscal first-quarter earnings for 2026 in the near future. Ahead of the event, analysts expect WTW to report a profit of $3.60 per share on a diluted basis, up 15% from $3.13 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion. Stock Index Futures Rally on Prospect of End to Middle East Conflict, U.S. Economic Data and Fed Speak in Focus Ignore the Panic and Buy the Dip in Micron Stock, Says Bank of America Stocks Climb on Hopes for an End to Iran War Get exclusive insights with the FREE Barchart Brief newsletter. Subscribe now for quick, incisive midday market analysis you won't find anywhere else. For the full year, analysts expect WTW to report EPS of $19.56, up 14.5% from $17.08 in fiscal 2025. Its EPS is expected to rise 13.2% year over year to $22.15 in fiscal 2027. WTW stock has underperformed the S&P 500 Index’s ($SPX) 17% gains over the past 52 weeks, with shares down 13.8% during this period. Similarly, it underperformed the State Street Financial Select Sector SPDR ETF’s (XLF) marginal gains over the same time frame. WTW's stock is under pressure due to mixed earnings, slowing revenue growth, and increased competition. Investors are also worried about AI disruption in insurance and brokerage, impacting broker valuations. Analysts’ consensus opinion on WTW stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 23 analysts covering the stock, 12 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and 10 give a “Hold.” WTW’s average analyst price target is $369.63, indicating a potential upside of 27.2% from the current levels. On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com